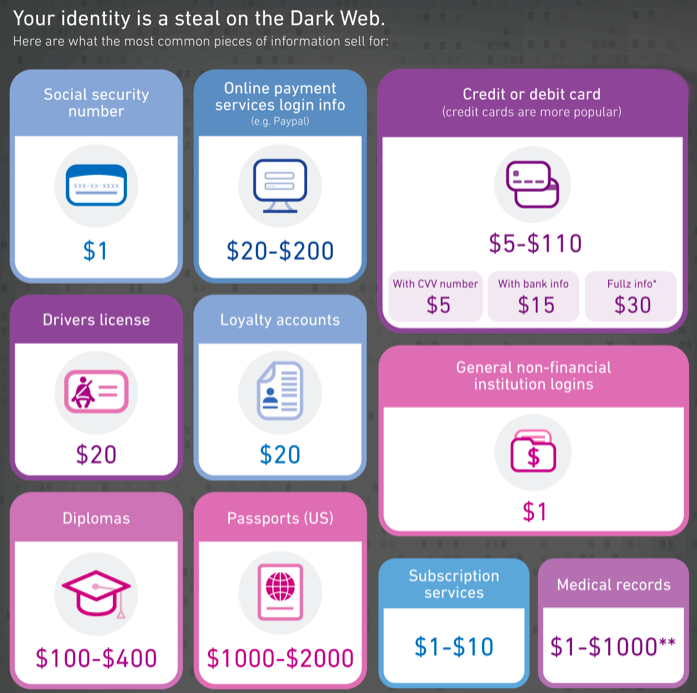

When the internet was launched in the 1990s, it felt safe behind the hide behind a veil of anonymity. Basically, nobody knew if you were a dog, however, in the 2020s online giants like Amazon, Google, Apple, Facebook (GAFA) are building user profiles. With the help of Artificial Intelligence and Machine Learning, they not only wish to offer product recommendations to their customers but also are keeping data that can trace behavior/purchases for more than a decade. know about how to dealing with identity management – KYC and AML(Identity theft).

We all to a point like the convenience of quick check-out while shopping online. However, these become easy gateways for fraudsters and scammers to hack your account and steal your information as well as identity. Know Your Customers (KYC) and Anti-Money Laundering (AML) compliances have become pivotal for not only banks and financial institutions but also for social media giants who must adhere to it. In order to meet the KYC/AML compliances, companies need to follow norms and maintain specific records of their customers to prevent money laundering, terrorist activities, and identity theft.

According to LexisNexis Risk Solutions, companies with less than US$1 billion in assets are spending US$850,000 as AML operational costs annually. Mid-tier firms expenditure on AML alliance is around US$7.4 million whereas the top tier firms with more than US$100 billion in assets spend an average of US$15.8 million.

Furthermore, in addition to the massive cost, the current KYC/AML processes contain certain inefficiencies, for e.g.:

- the KYC compliance duplication within and between FIs

- data’s between FIs and regulators are inconsistent, as updating data is a long and tedious process

- a large number of hours and resources are done via manual validation

The Blockchain helps to safeguard peoples’ identity and fasten KYC/AML.

Some good processes can be

- Real-time information updating -The current KYC checking as well as updating process takes around 5-6 days to fulfill the demands of the regulators. With a distributed ledger technology, the KYC process of days can be reduced down to minutes. Blockchains like Hyperledger can offer to develop a database that contains all the activities of a customer. This information can be made available to employees on network 24*7. Any updates or changes in a customer’s status could be communicated and updated in near real-time, as a result, it will be easy to catch a potential scam or fraudulent transaction.

- Data quality and governance: Information on the blockchain ledger cannot be altered easily. With the Hash protocol, any piece of information which is altered in a particular block can be tracked and monitored, thereby reducing chances of fraud and misuse. As of now, when it comes to financial institutions, information is stored in silos. A blockchain-based ledger can not only combine all the information on a single platform. With enhanced data governance, companies can zero-in fraudulent activities at an earlier stage as well as minimize fines levied due to compliance failures.

- Comprehensive authentication process: Blockchain technology offers decentralized solutions and at the same time ensures security protocols and regulatory requirements are met. Financial institutions will only be able to access client’s sensitive data with the help of cryptographic verification. As per the report of Goldman Sachs, Case Study 7, this can help the banking and financial sector to reduce 10% expenses. The cost-saving can go up to $160 million annually. Moreover, technology also lowers down the AML penalties between $0.5 to $2 billion dollars.

Author: Alessandro Civati – Copyright © 2020 All rights reserved – C.I.P. Ltd. (UK)